What is a SPAC?

A “special purpose acquisition company,” otherwise known as a blank-check company, is a public company created for the sole purpose of raising capital (through an IPO) in order to acquire or merge with a private company. The public company does not have any commercial operations, and its founders may not even be considering a specific acquisition target, which is why it is referred to as having a blank check. Private companies that use SPACs are typically smaller and not as attention-grabbing and exciting as technology startups, but they are still growing at solid rates and have high potential.[1]

What are the Advantages of Using a SPAC?

The usage of SPACs has become increasingly popular since 2011, accounting for 59 out of 235 total IPOs and raising $13.6 billion in 2019.[2] They’re popular for both business reasons and personal reasons. One advantage is that it is cheaper than a traditional IPO transaction. SPAC transaction fees usually consist of a 2% underwriting fee with an additional 3.5% underwriting fee that is paid by the company after the merger or acquisition.[3] Traditional IPO transactions, on the other hand, usually cost 7% of the capital raised during the process and must be paid by the company itself.[4] SPAC IPOs also take much less time to process (typically a matter of weeks) because the public company lacks commercial operations and filing is less complex, compared to a company using a traditional IPO (typically a matter of months).[5] This can be especially beneficial in a market that quickly grows and evolves, and it allows executives within the company to formulate a stronger plan to capture market share and spin it into action.

For CEOs, SPACs are attractive because they offer flexibility. According to Forbes, the CEO of a special purpose acquisition company only has to commit to a relatively short time frame and can focus his or her efforts in an industry sector where they are truly passionate.[6] And for investors, SPACs allow for greater input and control over important decisions as investors can cast votes in favor of or opposing a target acquisition.[7]

Content Preview

What are the Disadvantages of Using a SPAC?

While choosing to use SPACs may seem like a more efficient, cost-effective, and flexible strategy than a traditional IPO, SPACs still come with their own distinct disadvantages. The main issue with these entities revolves around various associated uncertainties and limits. For example, public shareholders of a SPAC have the option to trade in their shares for cash, which makes the ending amount of available cash unknown and difficult to predict.[8] Furthermore, there can be heavy repercussions if the deal falls through for any reason. If the public company fails to raise enough financing, deal protection can become scarce because the access to cash other than that raised by the deal is limited.[9] If the SPAC sponsors fail to target a specific private company and successfully merge with or acquire it before the deadline to liquidate, the funding is returned to stockholders and warrants become worthless.[10] This creates an environment of stress and pressure that may make it seem like SPACs are not worth the hassle.

Example 1: Nikola

On June 4th, 2020, the electric vehicle manufacturer and upcoming Tesla competitor, Nikola, went public via a merger with the SPAC VectoIQ Acquisition Corporation. Nikola’s listing on Nasdaq came under the ticker symbol NKLA at a price of about $34 a share. Nasdaq executive Eklavya Saraf remarked that SPACs provided “disruptive, forward-thinking companies” like Nikola with opportunities to seek capital, especially in difficult market conditions such as those caused by the coronavirus pandemic.[11] It’s interesting to note that Nikola, as innovative as it might seem, currently has an enterprise value of $23B (as of 06/18/20) despite having zero sales so far. This raises the question: will this set a precedent for even more companies—companies that have lofty ideas and promises rather than tangible products—to take advantage of SPACs in the future?

Example 2: Mature Unicorns

Activist investor and billionaire Bill Ackman revealed on June 22, 2020 that his hedge fund, Pershing Square Capital, would invest at least $1 billion into a blank-check company called Pershing Square Tontine Holdings.[12] According to the IPO Investment Prospectus, the SPAC is expected to offer 150 million shares at a price of $20 each and is said to target “mature unicorns.”[13] This term refers to private, highly entrepreneurial companies that have been financially successful in the past and have high growth potential in terms of improving its cash flow as well as bolstering its dominance in the market. The document also positions the coronavirus pandemic as a financial opportunity, rather than a threat, to Ackman’s firm. In a time of uncertainty and volatility, SPACs have become more attractive than traditional IPOs due to the greater decisiveness and shorter timelines associated with the merger transactions.[14]

Notable Companies That Have Gone Public Using SPACs

- Virgin Galactic (SPCE)

- DraftKings (DKNG)

- Hostess Brands (TWNK)

- Utz Quality Foods (to be expected, 2020)

Source: Barron’s[15], Wall Street Journal[16]

Conclusion

Special purpose acquisition companies can offer both cost and time advantages, as well as considerable amounts of risk. They’ve been popular for almost a decade, with the number of SPAC IPOs increasing every year, and have the potential to become even more popular in the future. Ultimately, it is up to the SPAC sponsors to decide whether the advantages outweigh the disadvantages or not.

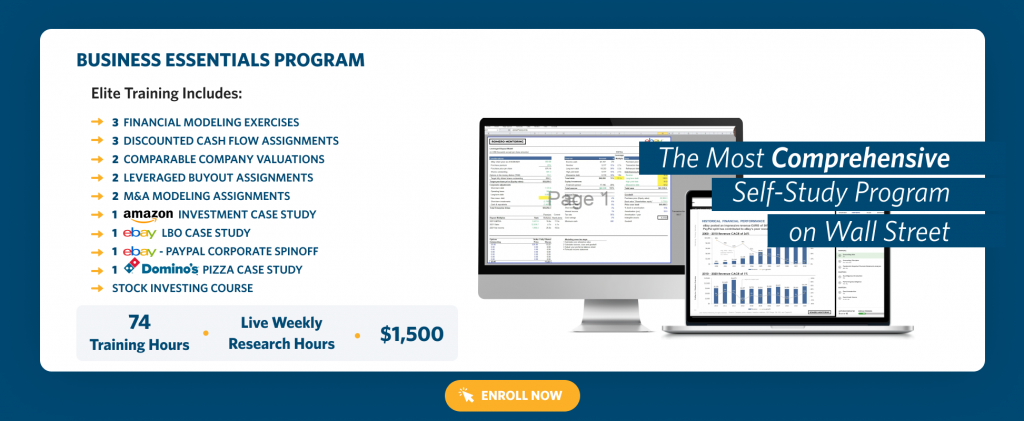

Romero Mentoring’s Analyst Prep Program

The Analyst Prep Program teaches the technical and practical skills that investment banks, hedge funds, and private equity & consulting firms look for in a candidate. Students begin with little to no technical skills and develop into fully prepared professionals who can perform as first-year analysts from day one through the program’s training and internship.

Our Story

Luis Romero, founder of Romero Mentoring, spent five years developing an analyst training program that he wishes he had when he was in college – especially one that gave him access to a complete training and finance internship experience that could advance his career. Since no opportunity like this existed to him at the time, Luis went through a stressful recruiting process like so many others have. He successfully landed a full-time job offer upon graduation and worked as an M&A analyst at Credit Suisse in NYC for two years. He then moved to the buy-side as a junior trader and analyst. After gaining experience there, he created his own fund, Romero Capital, and later become an instructor in financial modeling and valuation. After working with hundreds of professionals and analysts, Luis became committed to creating his own mentoring program because he understood the crucial need for a hands-on, personal experience in the competitive world of finance.